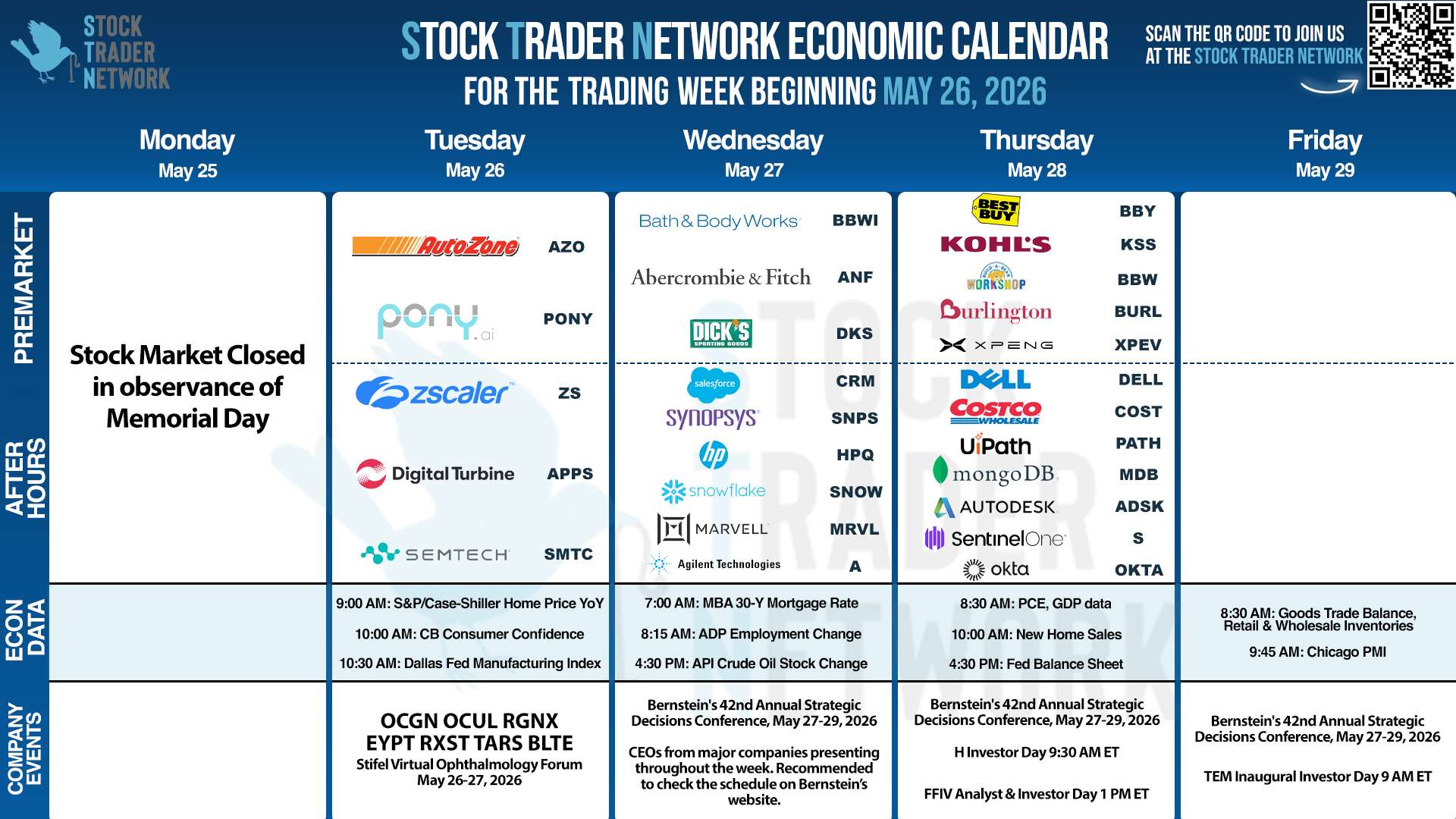

May 26–29, 2026

Markets head into the week with a shorter but important macro calendar, and a decent earnings slate. The other thing hanging over the tape is the Strait of Hormuz. Shipping has started to move again, oil has come off its highs, and the market is trading as if a broader disruption may be fading, but the diplomatic picture still looks fragile enough that headlines can move it.

Upcoming Earnings:

Tuesday, May 26

- AutoZone (AZO) — Before Open

- Zscaler (ZS) — After Close

Wednesday, May 27

- Dick’s Sporting Goods (DKS) — Before Open

- Abercrombie & Fitch (ANF) — Before Open

- Snowflake (SNOW) — After Close

- Salesforce (CRM) — After Close

- Marvell Technology (MRVL) — After Close

- HP Inc. (HPQ) — After Close

Thursday, May 28

- Dollar Tree (DLTR) — Before Open

- Costco Wholesale (COST) — After Close

- Dell Technologies (DELL) — After Close

- MongoDB (MDB) — After Close

- Okta (OKTA) — After Close

- UiPath (PATH) — After Close

- Autodesk (ADSK) — After Close

Economic Data (ET)

Tuesday, May 26

- 10:00 – Consumer confidence (May)

Thursday, May 28

- 8:30 – Weekly jobless claims

- 8:30 – Durable goods orders (Apr)

- 10:00 – New home sales (Apr)

Friday, May 29

- 8:30 – GDP, second estimate (Q1)

- 8:30 – Personal income and PCE (Apr)

- 9:45 – Chicago Business Barometer (May)

Fed Speakers (ET)

Wednesday, May 27

- Lisa Cook, Fed Governor — Speech: AI, the Economy, and the Financial System (3:55 p.m.)

- Philip Jefferson, Vice Chair — Discussion: Global Economic Developments and the U.S. Economy (8:00 p.m.)

Friday, May 29

- Michelle Bowman, Vice Chair for Supervision — Speech: Reykjavik Economic Conference 2026

Why This Week Matters:

The macro side is back-loaded. Tuesday brings durable goods, home prices and consumer confidence, but Thursday is the event with the second look at first-quarter GDP, April personal income and PCE, plus housing data from both new and pending home sales.

The Strait of Hormuz is the swing factor sitting around all of this. Reuters reported Sunday that several oil and LNG tankers have now exited the strait, while the AP said markets were rallying on expectations that negotiations could reopen the passage more fully and calm the energy shock.

At the same time, Reuters reported Friday that the emerging U.S.-Iran understanding was only “largely negotiated,” which is another way of saying it is not done yet. That matters because every step toward normalized traffic helps the inflation story, and every setback risks pushing oil and broader risk sentiment the other way again.

On the corporate side, Salesforce and HP report Wednesday, Marvell joins them after the close, and Thursday brings Dell, MongoDB and Costco. Salesforce matters because software has been trying to regain its footing, Marvell and Dell matter because they sit in the AI hardware buildout, MongoDB gives the market another test of how investors are pricing software in an AI-disruption world, and Costco remains one of the cleanest reads on the higher-income consumer.

Want this newsletter delivered straight to your inbox before the week starts? Sign up for STN or enter your email here.